Competitive Edge

February 8th, 2023

Have another North American port you would like for us to track weekly? Email us at [email protected]

Takeaways

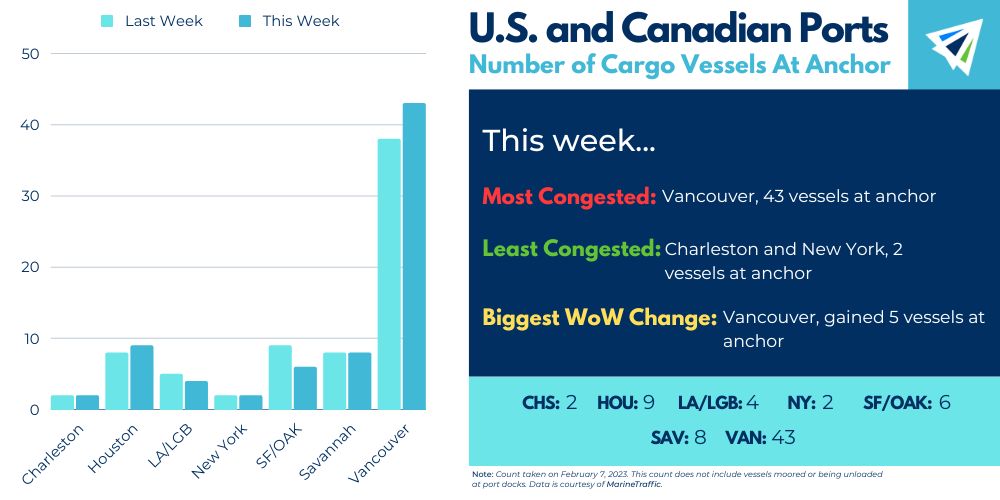

• U.S. West Coast: Three things seem inevitable in life–death, taxes, and stalling contract negotiations. Until resolved, the WC’s freight share will continue to hemorrhage as shippers remain averting.

• U.S. Gulf Coast: The Gulf Coast port’s dwell fee program went into effect February 1. The Port of Houston will charge $45 per unit per day to cargo owners if a container lingers more than eight days.

• U.S. East Coast: Charleston, New York, and Savannah all reaming in single-digits and have observed no week-over-week change. This is also the second-straight week that Savannah and New York have both stood put at only two vessels anchored offshore.

IMPORT: Asia to North America (TPEB)

Recent Developments:

• Chinese New Year’s typical celebration period wrapped up Sunday, February 5. Manufacturing, production, and full port operations are expected to resume this week.

• West Coast contract negotiations between the International Longshore and Warehouse Union (ILWU) and Pacific Maritime Association (PMA) remain active. The existing labor contract between the two parties expired July 1.

Rates: Rates to all US coasts have leveled as we depart from CNY.

Space: Space is open.

Capacity: Capacity is open and increasing over the next few weeks. However, there is some carrier aggression with blank sailings to combat this.

Equipment: For the most part, there is availability at inland and coastal ports.

TIPS:

• Book at least two weeks prior to the ready date.

• Expect blank sailings to carry on through Q1 2023.

IMPORT: Europe to North America (TAWB)

Rates: With capacity increasing and demand dropping, rates remain falling for this trade. However, they are still almost triple what they were pre-pandemic.

Space: Space to both U.S. coasts have opened up as U.S. congestion is minimal.

Capacity: Larger vessels have entered the market boosting the trade lane’s capacity. The 2M Alliance (Maersk and MSC) are announcing additions of even more market capacity.

Equipment: Availability has improved on both sides of the trade.

TIPS:

• Book at least three weeks prior to ready date.

• Even as market conditions become more fair, premium services (i.e., no-roll options and improved cargo reliability) should still be considered.

EXPORT: North America to Asia

Recent Developments:

• Agriculture exports typically begin picking up around this time of year. While this could present a surge in outbound volume, capacity will be expected to remain plentiful.

Rates: Rates are stable if not slightly decreasing. Though, they are not plummeting in this market like its inbound counterpart (Asia to North America).

Capacity: Capacity is widely available for all services. Aside from possible blank sailings in February, no considerable changes to this market’s capacity in the near future.

Equipment: Most inland and coastal ports have balanced out their equipment availability. No outstanding challenges to U.S. availability to report as of now.

TIPS:

• Book at least three weeks prior to the time of departure.

• While not as frequent as its inbound counterpart, remain in close contact with your providers to be aware of any potential developments, like blank sailings.

• Shippers with high volume projects should take advantage of carrier receptiveness to take on these opportunities. Space is wide open with a high acceptance rate.

InterlogUSA Proudly Presents...Freight FM Ep. 5: Discussing the China Trade Lane

In our latest episode, InterlogUSA’s Rachel and Madison discuss the China trade lane and what importers can expect after Chinese New Year.

If you are a China importer, you’ll want to check this episode out!

“Freight FM” features short-form video interviews with InterlogUSA’s industry experts offering insights into breaking news, market trends, our company’s history, and more!

In The News: A Train Derails Throughout Eastern Ohio and Pennsylvania

You may have seen in the news about a Norfolk Southern train that derailed close to Ohio village of East Palestine back on February 3rd, which triggered a fire.

The cars were carrying vinyl chloride – a hazardous commodity.

NS released a statement saying shipments are being delayed through an area from Chicago to New York and Kansas City while workers attempt to clear the scene.

Freight News

U.S. Import Outlook Through the First Half of the Year Remains Gloomy

The National Retail Federation (NRF) anticipates that U.S. imports through the first half of 2023 will fall around 20 percent, from the same timeframe last year.

Currently, projections regarding February imports are expected to be 25.5 percent lower than a year ago – which is a slight downgrade from last month’s projection of a 23 percent drop.

Additionally, February’s projected import number is 1.57 million TEU (twenty-foot equivalent units) and would be the lowest for the U.S. since May 2020. Note: May 2020 was during the pandemic, which was a significant period for the industry. During which the supply chain throughout the world became abnormal from years prior, so keep that in consideration with this stat.

Right now, experts are seeing retailers be cautious…as they “wait and see” how the economy responds to efforts in bringing inflation under control.

Furthermore, June is the expected month where any “real” improvement will be noticeable in regards to imports, per the Journal of Commerce. Obviously things can change and perhaps more improvement will be made before then, or vice versa.

After a Four Month Hot Streak, the Port of New York and New Jersey See Volumes Dip YoY in December

Last year was a pretty good year for the Port of New York and New Jersey as they experienced (and celebrated) record volumes – included a four month hot streak as the United States busiest container port.

That hot streak ended in December, as cargo volumes fell nearly 21 percent year-over-year to 613,011 TEUs – Supply Chain Dive reports. The port remained the nation

Though, throughout 2022, the Port of NY/NJ moved a record total of nearly 9.5 million TEUs – the first in their Port history.

Recently, the Port of NY/NJ had their State of the Port briefing, with the Port Director, Beth Rooney, saying, “there is no longer any seasonality or predictability to the cargo peaks and valleys that our industry had become accustomed to.”

Rooney expects the market to remain soft but at more normalized levels through the first half of the year.

Watch Our January Webinar!

We discussed the impact of zero COVID policy suspension in mainland China before the Chinese New Year holiday, CNY impacts, carriers’ blank sailings before/after CNY timeframe, and the 2023 China Ocean Market Outlook.

Sign Up for Next Month's Webinar

Our next webinar will be on Wednesday, February 15th!

Some topics that we will discuss:

-RFQ’s: what shippers should keep in mind as we head into the season of RFQ’s, are RFQ’s this year going back to what they were pre-pandemic?

-Post Lunar New Year: what do rates/capacity look like this month?

-Current events

We would like to hear from you. If you have any questions or topics you would like our experts to discuss in future webinars, please let us know!

Interlog  Insights

Insights

Last week’s newsletter was the first one of February!

We discussed how some shippers are cautiously optimistic ahead of a soft freight market, schedule reliability throughout the U.S., and an update on the Port of Houston’s dwell fee.

Don’t forget to sign up so you can receive upcoming insights!

Sign up for our

industry answers

Our team works to provide valuable, unique, and relevant content to assist you in finding solutions. Sign up now.