Competitive Edge

February 15th, 2023

Have another North American port you would like for us to track weekly? Email us at [email protected]

Takeaways

• U.S. West Coast: While vessel congestion remains an issue of yesteryear for the USWC, the coast’s outstanding dockworker contract talks has presented their own challenges.

Dockworkers and marine terminal employers have resumed negotiations the other week after agreeing to set aside (for now) a controversial jurisdictional issue involving Terminal 5 in Seattle. This dispute has greatly contributed to the lack of progress over the past nine months.

• U.S. Gulf Coast: The Gulf Coast port’s dwell fee program went into effect February 1. The Port of Houston will charge $45 per unit per day to cargo owners if a container lingers more than eight days.

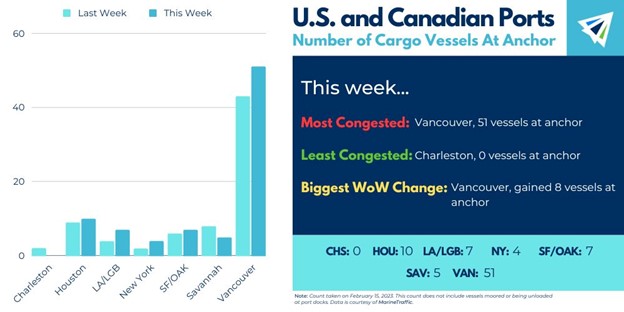

• U.S. East Coast: Charleston dons a “donut” this week with zero vessels anchored off its shore. New York and Savannah follow a similar suit and have stayed in the single-digits.

After a successful 2o22, Where New York saw itself leading the country in volumes for a good stretch, the EC hub is now seeing a dip in the amount of cargo coming through.

While the EC continues to benefit from more freight share as shippers remain averting the WC, low overall demand from U.S. importers has impacted the throughputs of all American ports, including the EC.

IMPORT: Asia to North America (TPEB)

Recent Developments:

• Any Chinese New Year- related impacts on the market have settled. Rates remain soft, capacity is widely available, and space is open.

• Carriers remain aggressive with blank sailings and general rate increases to buff up and stabilize low rates.

• West Coast contract negotiations between the International Longshore and Warehouse Union (ILWU) and Pacific Maritime Association (PMA) remain active. The existing labor contract between the two parties expired on July 1, 2022

Rates: Rates to all US coasts are low and level.

Space: Space is open.

Capacity: Capacity is open. However, expect more incidences of blank sailings from carriers.

Equipment: For the most part, there is availability at inland and coastal ports.

TIPS:

• Book at least two weeks prior to the ready date.

• Expect blank sailings to carry on through Q1 2023.

IMPORT: Europe to North America (TAWB)

Rates: With capacity increasing and demand dropping, rates remain falling for this trade. However, they are still almost triple what they were pre-pandemic.

Space: Space to both U.S. coasts have opened up as U.S. congestion is minimal.

Capacity: Larger vessels have entered the market boosting the trade lane’s capacity. The 2M Alliance (Maersk and MSC) are announcing additions of even more market capacity.

Equipment: Availability has improved on both sides of the trade.

TIPS:

• Book at least three weeks prior to ready date.

• Even as market conditions become more fair, premium services (i.e., no-roll options and improved cargo reliability) should still be considered.

EXPORT: North America to Asia

Recent Developments:

• Agriculture exports typically begin picking up around this time of year. While this could present a surge in outbound volume, capacity will be expected to remain plentiful.

Rates: Rates are stable if not slightly decreasing.

Space: Space is wide open.

Capacity: Capacity is widely available for all services. No considerable changes to this market’s capacity through Q1, 2023.

Equipment: Most inland and coastal ports have balanced out their equipment availability. No outstanding challenges to U.S. availability to report as of now.

TIPS:

• Book at least three weeks prior to the time of departure.

• Blank sailings have not been routine for the market but remain in close contact with providers to be aware of any developments.

• Shippers with high volume projects should take advantage of carrier receptiveness to take on these opportunities. Space is wide open with a high acceptance rate.

InterlogUSA Proudly Presents...Freight FM Ep. 5: Discussing the China Trade Lane

In our latest episode, InterlogUSA’s Rachel and Madison discuss the China trade lane and what importers can expect after Chinese New Year.

If you are a China importer, you’ll want to check this episode out!

“Freight FM” features short-form video interviews with InterlogUSA’s industry experts offering insights into breaking news, market trends, our company’s history, and more!

U.S. DOT Announces Over $600 Million in Grants for U.S. Port Projects

The U.S. Department of Transportation has allocated $662 million in grants, which are available for port infrastructure projects throughout the 2023 fiscal year.

One hope, the U.S. DOT has, is for some of this funding to go towards some projects to be created that will help reduce carbon emissions at ports.

Additionally, in the next few weeks, the Federal Highway Administration will open their own grant program that will be used for testing, evaluation, and deployment of electrification projects that will be aimed at port trucking, per the DOT.

Freight News

U.S. Container Import Volumes in January see 2019 Levels

U.S. container import volumes in January this year have aligned very close to pre-pandemic (2019) numbers.

Specifically, in January 2019, total U.S. container import volumes were 2,074,717. While in January 2023, that total was 2,068,493 – per data from Descartes. As you can see, these totals are very similar. When you look at what volumes were like in December 2022, the total was 2,466,015 – which is 397,522 more than the totals in January this year.

The U.S. East and Gulf Coast ports continue to see port transit times dip, while transit times out of the West Coast are increasingly, slightly. The slight increase in port transit times is mainly due to the unresolved labor – related issues that have kept some importers from shifting some volume back to the West.

USWC Labor Talks Continue - What Do We Know So Far?

Contract negotiations involving dockworkers and marine terminal employers out on the U.S. West Coast have resumed, after they agreed to temporarily set aside a jurisdictional issue that involved Terminal 5 out in Seattle.

You can read more about that dispute, here.

Many in the industry view the resumptions of these negotiations to be a significant development, the Journal of Commerce reports.

It also should not be forgotten that both sides may be feeling some ‘external pressure’ to get a deal put together. It is to be said that port and terminal stakeholders are getting impatient by cargo continuing to shift out of the USWC, with shippers concerned about potential disruption linked to the contract talks.

Watch Our February Webinar!

Topics:

- CNY/Trade Lane Predictions

- Blank Sailings

- Benefits of Outsourcing Your Logistics

Sign Up for Next Month's Webinar

Our next webinar will be on Wednesday, March 15th!

We would like to hear from you. If you have any questions or topics you would like our experts to discuss in future webinars, please let us know!

Interlog  Insights

Insights

Last week’s newsletter, we discussed how carriers are shifting capacity to the Trans-Atlantic market, plus what will drive the cold chain market this year?

Don’t forget to sign up so you can receive upcoming insights!

Sign up for our

industry answers

Our team works to provide valuable, unique, and relevant content to assist you in finding solutions. Sign up now.