Interlog  Insights

Insights

February 2023

The following is an archived collection of our weekly insights through the second month of 2023. Those who had signed up to our Interlog Insights newsletter received each week’s update to their inbox on the original release date. If you like what you see below, please feel free to sign up yourself to get these updates right as they come!

This month's insights

- 1H 2023 Volume Forecasts

- Ocean Freight Capacity

- Cold Chain Growth Drivers

- 2M Termination

Week 4 - Originally released February 24

Recap: Insights We've Covered in February

At the beginning of the month, we provided an update on the Port of Houston’s sustained import dwell fee that officially went into effect February 1. As of now that fee is still occurring. Also, in our February Insights we discussed how schedule reliability in the U.S. has seen some slight improvements. We then switched it up a little bit and discussed the top four cold chain growth drivers – food supply outsourcing, food waste mitigation, decarbonization goals, and technology – for 2023. The cold chain is a crucial part in delivering perishable products in a safe and high quality way for consumers. Like most things, better communication could be helpful in mitigating the losses reefer businesses have – as between 7 and 15 percent of food transported in reefer containers become inedible by the time it has reached its final destination. If you have any industry topics or news that you would like our experts to discuss in our newsletter, please tell us know. We want to make sure our viewers get the most out of this newsletter, so if there is a topic, please share it with us at support@interlogusa.com. |

For a closer look at the details behind the decision to terminate the 2M Alliance and what a post-2M shipping landscape will be like for Maersk and MSC, please refer to our blog.

Insight: 2M Termination - Will there be a ripple effect?

Over the course of February, we’ve discussed cautiously optimistic shippers, inbound volume forecasts for the first half of 2023, and carriers shifting capacities from the Pacific to the Atlantic. While freight activity is muted right now, the industry has been awfully noisy as it situates itself in what appears to be a post-pandemic, new normal, era for international shipping. It doesn’t take astronomically high demand, chokehold capacity, or various supply chain bottlenecks to keep stakeholders on the move. Whatever the market looks like, we’ve all learned complacency will be anyone’s downfall in our industry. In what felt ceremonious ahead of this new era, the world’s two largest ocean liners decide to terminate their crowned 2M Alliance. The mutual decision to part ways and, in their words, pursue different individual strategies was fueled from the immense growth the two carriers each enjoyed over the last two years. MSC and Maersk both reaped insane profits and, respectively, flipped them for more ocean capacity (MSC) and full end-to-end logistics operations (Maersk). With one set to conquer ocean freight and the other set to embed itself in every nook and cranny of transportation, the soon-to-be-divorced allies are apparently confident enough to bypass alliance formality. That said, does the termination of 2M (effective January 2025) signal other alliance breakups or shifts down the road? At this point in time, we don’t foresee any dramatic breakup or shuffling of major alliances, like Ocean Alliance or THE Alliance. Other ocean lines are not as big as MSC or Maersk. While they could shuffle around, it’s likely not practical right now for many of them to break off their agreements and enter free agency. However, in terms of the decision’s precedent, spilt water never returns to the cup. 2M’s termination introduces our industry to one of the first examples of post-pandemic direction. It’s naïve to assume other carriers aren’t taking note of this development and thinking if a similar move from their end is advantageous. While MSC’s orderbook dwarves any of its competitors, other carriers have invested in expanding ocean capacity. While Maersk has made huge acquisitions to satisfy end-to-end operation, other carriers have been active as well in the name of similar ambitions. In other words, carriers recognize an alliance-free operation could be an ideal direction to take, however, practically speaking, many of them are not able to stand alone with their service networks alone. At least, not without sacrificing quality and coverage. |

Week 3 - Originally released February 17

Insight: Import Volume Forecast for the First Half of 2023

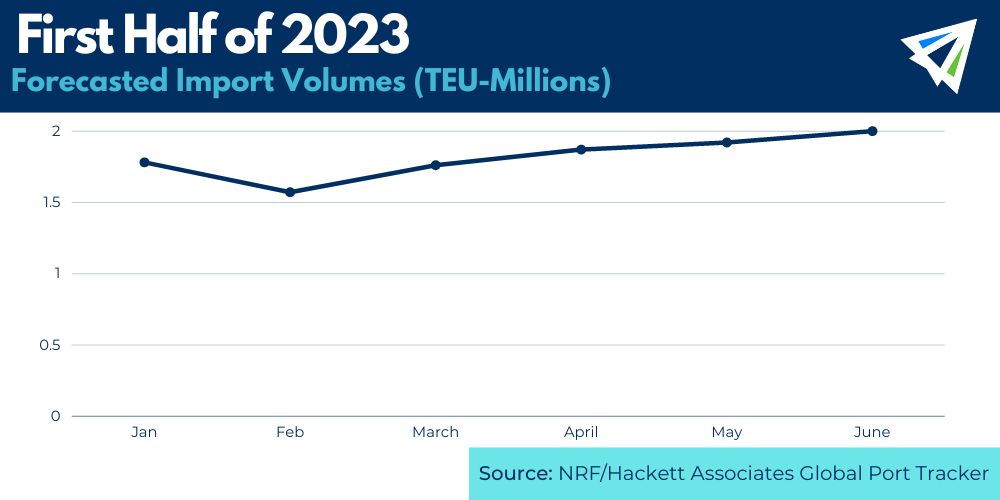

The word is out. January’s U.S. import volumes are in. Drum roll. Courtesy of data from Descartes, inbound freight rolled through at 7.2 percent jump compared to December with over 2 million TEUs entering our country’s hubs. That said, containerized imports registered their highest month-on-month gain since last May! Whoa! Low demand, who? Were we premature to think demand in the first half of 2023 was going to be a quiet affair? Batton the hatches, we are in for another freight surge. Right? Unfortunately, none of that’s the case. Despite the monthly gain, demand was low through January and will be slotted to stay low into February. In fact, January’s numbers in the new year closely mirror pre-pandemic volumes from January 2019 and 2020. February volumes are forecasted to be the lowest in nearly three years So, what do we make of this volume uptick then? Is it simply a blip or can we expect this momentum to hold going into February, March, and so on? To answer these questions. No, January was not a blip and we do suspect there to be positive, yet modest, inroads to currently waned demand through the first half of the year. However, it’ll have to wait one more month. According to the National Retail Federation’s Port Tracker, import volumes for February are expected to be the lowest since May 2020.

|

First half outlook for 2023 sees a plunge in February for import volumes. From there, volumes look to gradually rise through June.

Uncertain economy plays a role in second half of the year outlook

After February, it does appear import volumes will start their crawl from the basement to levels that soar comfortably above 2019 data.

By the time the second half of 2023 rolls around, we will be anxious to see whether volumes will reside around pre-pandemic levels or if they climb enough to flirt with historical levels seen widely throughout 2021 and early 2022.

While current volumes reflect pre-pandemic times, what’s different this time around than four years ago is the uncertainty of the economy. Arguably the biggest driver in import growth, it’s hard to pinpoint how the American economy is going to fare later in the year and, in return, the extent to which demand will grow.

Week 2 – Originally released February 10

Insight: What Will Drive the Cold Chain Market in 2023?

The cold chain – somewhat self-explanatory – refers to managing the temperature of perishable products in order to maintain quality and safety from the point of origin through the distribution chain to the final consumer – as defined by the Global Cold Chain Alliance. And, the supply chain plays a crucial role in delivering those perishable products in a safe and high quality way for consumers to consume. Thus, improving the cold chain fluidity does not “just happen” it needs investment and innovation. That leads us into… The top four cold chain growth drivers for this year: Food supply outsourcing The food industry is an industry that will never go away, which means demand will always be high. So, as the world’s population continues to expand, so does the advancement of food being transported safely and swiftly. Refrigerated equipment, such as equipment that includes telematics, is important in the transport journey because it can ensure that the cargo is handled thoroughly the entire way. Furthermore, the reefer market is expected to grow on an average five percent year-over-year through 2025, while breakbulk container demand is anticipated to drop 15 percent, GCCA reports. Food waste mitigation Food waste in the supply chain continues to be an issue and is expected to be an even bigger problem this year. As mentioned above, telematics technology would allow for an increase in transparency and real-time data. This would allow for more accurate information on the exact location of the container, which is crucial for proper planning, and ultimately can help eliminate some food waste. Decarbonization goals Innovation and being open-minded are keys to reaching decarbonization goals. Some things up for consideration when reducing greenhouse gas emissions are variable speed drives for compressors and two-speed evaporator fans – which offer energy efficiency and can elevate even the most optimal operation linked to an energy-efficient fleet. Technology Technology will be used to map the entire end-to-end supply chain more accurately. GCCA expects advancements in technology, digitalization and the digital transformation of businesses to be drivers of growth, not just for the reefer market but for the overall supply. In summary The cold chain is a huge part of the food industry and making sure those shipments are packed correctly and the container temperature is accurate is crucial, so the food does not spoil – thus, creating food waste. This year the top four cold chain growth drivers are food supply outsourcing, food waste mitigation, decarbonization goals, and technology – with each being a vital part of improving the cold chain this year. |

Insight: Capacities Have Shifted to the Atlantic as Carriers Eye Higher Rates

Last week, the subjects of our focus were the cautiously optimistic importers ahead of a soft transpacific market. This week, we are shifting to another trade. The transatlantic market. As a reader of a sign-up logistics newsletter, we know you know all things in our industry ebbs and flows. Right now, transpacific trade is soft. Inbound volumes, at least leading up to January, were playing a competitive game of limbo—how low could they go?—and remain remarkably low as we speak. Such little volume caught carriers dangling with overcapacity. In return, this led to these carriers, who once salivated at the profitability of transpacific imports, to rethink their capacities. In other words, where can we make the most money? In fact, according to FreightWave’s SONAR indexes, spot rates from Europe to the East Coast remain almost triple what they were pre-pandemic and more than triple what current transpacific (Asia to the West Coast) spot rates are going for. Many major shipping lines, like Cosco and ONE, have upped sailing frequencies of their respective Europe-East Coast services while some swapped in goliath-sized ships. Take for instance, Evergreen. The Taiwanese carrier’s Tampa Triumph was introduced to the trade last December. The ship has a whopping 14,000 TEU capacity. Moves from carrier alliances as well highlight the shift to the Atlantic. THE Alliance and Ocean Alliance reinstated calls in key East Coast hubs, like New York and Savannah, while the 2M Alliance added more ships to its network. Could this shift drive down transatlantic rates? With more ships entering the market, are these higher rates going to plummet as a result? We want to say it’s ironic that carriers shifting their vessels over to Atlantic to chase a more lucrative market may be the reason to drive these high rates down, but that just wouldn’t be the case. In reality, it’s the appropriate reaction for when more supply is brought into the market. For the foreseeable future, rates will remain considerably higher when compared to the transpacific. However, the influx in capacity coupled with demand dipping the last couple of months has prompted spot rates to steadily decline. In 2022, a volume driver for European imports was the edge the U.S. dollar had on the euro. In recent months, the euro has made inroads on the USD in strength and this currency advantage for importers has waned. We anticipate a sustained downward trend in rates for the transatlantic. |

Week 1 – Originally released February 3

Insight: Inside the Mind of the Cautiously Optimistic Shipper

Out with the new, and in the with old? For transpacific inbound trade, current spot rates are grazing pre-pandemic levels and vessel space is wide open for the taking. For any supply chain veteran, this looks familiar to how conditions were prior to the pandemic. It may appear our industry has finally turned the corner from a strange and volatile three-year blip. However, many shippers remain cautiously optimistic ahead of what seems like a jaunt back to market normalcy. Despite a soft market, shippers zero-in on the big picture

|

Insight: Port of Houston's Sustained Import Dwell Fee is Now in Effect

As we mentioned in week one of last month’s Insights, we discussed that the Port of Houston’s sustained import dwell fee would be implemented at the start of February.

This $45 per container per day fee is directly assessed to the BCO’s (Beneficial Cargo Owners) on the eighth day after the expiration of free time. You can read more about the fee here.

Insight: Schedule Reliability in the U.S. Sees Slight Improvements

Throughout the U.S. West Coast, scheduled reliability in December showed improvements – just slightly at 0.6 percentage points, compared to November 2022, per Sea-Intelligence.

But, the year-over-year gain was much higher (31.4 points) compared to the 9.7 percent that was recorded at the same time in 2021.

Scheduled reliability on the U.S. East Coast in December increased nearly 2 percentage points (1.7) over November, to 37.2 percent.

But year-over-year reliability was up around 18 percentage points from the 19.1 it received in December 2021.

For more expert discussion on market conditions for importers, please watch our February webinar. We touched base on post-Chinese New Year trade outlook and the benefits of outsourcing logistics.

What did you think?

In addition, please email us at sales@interlogusa.com with any news or topics you’d like our experts to cover in future issues!